Affordability for a house depends on several factors and varies greatly by location. Here’s a breakdown to give you a general idea:

Factors impacting affordability:

- Income: This is the most crucial factor. The higher your income, the more house you can potentially afford.

- Debt-to-Income Ratio (DTI): This ratio compares your monthly debt payments (including future housing costs) to your gross monthly income. Aim for a DTI below 36%, with some lenders allowing up to 43% in specific situations.

- Down Payment: A larger down payment significantly reduces the amount you need to borrow and lowers your monthly mortgage payment.

- Interest Rate: The interest rate on your mortgage significantly impacts your monthly payment. Lower rates mean you can afford more house.

- Property Taxes and Homeowners Insurance: These ongoing costs add to your monthly housing expense. They can vary significantly by location.

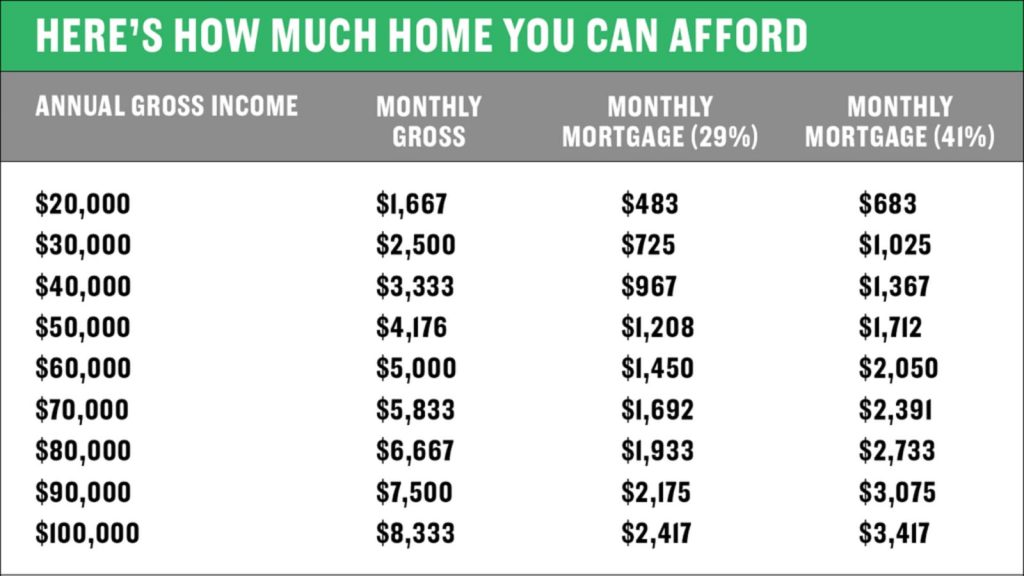

Rules of thumb (for informational purposes only):

- 28/36 rule: This common guideline suggests spending no more than 28% of your gross monthly income on housing expenses (including mortgage, property taxes, and homeowners insurance) and no more than 36% on total debt (including housing payment and other debts).

Resources to estimate affordability:

Online Mortgage Calculators: These let you input your income, estimated down payment, and desired loan term to see an estimated monthly payment:

https://www.latimes.com/projects/socal-home-mortgage-calculator-map

https://www.nerdwallet.com/mortgages/mortgage-calculator

Mortgage Pre-Approval: Getting pre-approved allows you to know exactly how much a lender is willing to loan you.

General affordability range (with caution):

While it’s difficult to pinpoint an exact range, nationally, a person making a median household income (for example around $67,500) and following the 28/36 rule might generally afford a house in the range of $250,000 to $400,000 (depending on other factors). However, this is a very broad estimate and location can significantly impact affordability.

Remember:

- Affordability is highly dependent on your specific situation.

- These are just estimates – getting pre-approved for a mortgage will give you a more accurate idea of what you can afford.

- It’s wise to be conservative with your estimates. Unexpected costs can arise, and you don’t want to be house poor (spending a majority of your income on housing).

For a more specific answer: